Updated on: February 14, 2025 | Article No: 294 | By: @rprasanth_kumar

People often ask me about various options in France for savings, investments, tax reductions, etc. and it is one of the most common FAQs. So, I started sharing regular updates on my personal finance portfolio since 2022. This can serve as an excellent guide for people, who are beginning their savings and investment journey. However, it should not be considered as an investment advice because I am simply sharing my own personal DIY experiences.

Here is my personal savings and investment portfolio updated until December 2024. I use google sheet and google finance formulas for tracking my portfolio.

Topics Covered 📚

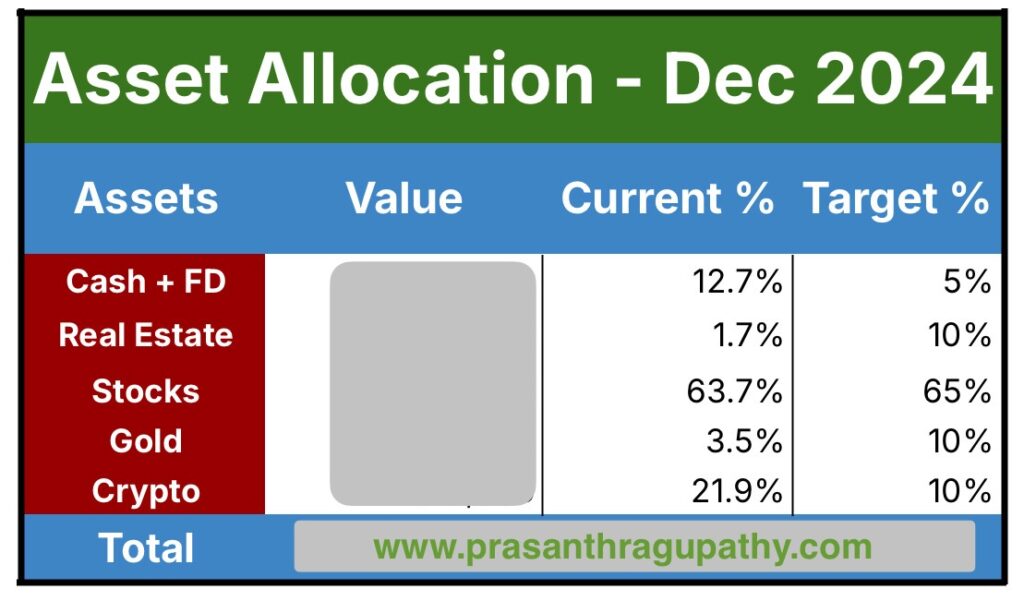

Asset Allocation

Let me start with the most important aspect of any personal finance portfolio: Asset Allocation. My target and current asset allocations are explained below. Due to the recent Crypto bull market, it is little out of order. So, 2025 is going to be a year of rebalancing for my portfolio.

Here is an excellent article about asset allocation from Investopedia: What Is Asset Allocation and Why Is It Important?. You can find detailed explanations of most of the topics mentioned further in the article and the personal experiences shared by other expats in a dedicated group India – France: Savings, Investments & Taxes – Discussions

An important piece of information is that I keep very little cash in my current accounts. All the month’s fixed and variable expenses, monthly investments, etc. are completed before the 10th of the month.

Bank Accounts

Another obvious and basic thing required to maintain our personal finances every day are our bank accounts. In general, an average person requires 2-3 bank accounts to manage their various activities.

- Primary account(s) to receive salary, business income, manage loans, monthly fixed expenses, etc.

- Secondary account(s) for day-to-day expenses, groceries, online shopping, etc.

Bank Accounts in France: Each bank account is meant for a specific purpose. Also, I try to use Apple Pay as much as possible to avoid any card scams, etc.

- For an overview of banking options in France, please refer to Banking:

- Opening a Bank Account in France.

- I have never paid any banking charges in France because I had the BNP Paribas student account free for 3 years. After graduating and finding a job, I moved 100% to online-only banks.

- So, all bank accounts are completely online and so I pay zero banking charges including the premium credit-cum-debit cards. Even the loan paperwork is done almost completely online. More details in Best Online Banks in France: Bourso Bank vs Hello Bank vs Fortuneo.

- One major drawback is that French online banks do not have any English-speaking customer care. But, almost everything can be done via the mobile app and the bank’s website. It is not a big issue but can test your patience sometimes.

- I can speak French, so I have zero complaints so far.

| Bank Accounts | Comments |

| Hello | Primary current & savings account. Opened as a student account with BNP in 2015. Transferred to Hello in 2018. Has more features than Bourso and the 3rd largest online bank in Europe. DM for referral with your Email ID. |

| Bourso | Primary current account for Salary & monthly fixed expense payments. Largest online bank in Europe. Referral Code: PRRA2704 |

Bank Accounts in India: Non-resident Indians (NRIs) and PIOs are not legally allowed to maintain normal resident bank accounts in India. These resident accounts must either be converted to Non-resident ordinary (NRO) bank accounts or closed.

- We can also open Non-resident External (NRE) bank accounts for sending our foreign income to India and use the NRO accounts for any income arising in India.

- An NRO bank account is mandatory for receiving income tax refunds in India.

| Bank Accounts | Comments |

| HDFC (NRE) | For Fixed Deposits, MFs, UPI payments, etc. |

| HDFC (NRO) | For Fixed Deposits, MFs, UPI payments, income tax declaration and refunds, etc. |

Note: I had opened a NRE bank account in 2018 with Kotak Mahindra Bank. It was opened directly from Toulouse (France) and the bank arranged a free pickup of documents via DHL. But their customer service was very pathetic and so I moved to HDFC Bank. Opened the account by visiting the local branch directly, during a trip to India in 2022.

Support This Blog!

If you’ve found my articles helpful, interesting or saving your time and you want to say thanks, a cup of coffee is very much appreciated!. It helps in running this website free for the readers.

Brokerage Accounts for Investments

Here is a list of my various brokerage accounts which I use to invest in stocks, ETFs, mutual funds, and cryptocurrencies. If interested, you can open your accounts by clicking on the links below.

Accounts in France: These accounts have been chosen based on various factors including fees, functionalities, availability of required fund choices, etc.

| Banks / Brokerages | Accounts & Comments |

| PEA. A primary investment brokerage account with tax advantages. Referral code: 2020751090 | |

| Bourso | Primary bank account and my PERin retirement savings account. Referral Code: PRRA2704 |

| Kraken | Cryptocurrency exchange account |

| CTO. Regular stock brokerage account. Interactive Brokers is a really good option too. |

Accounts in India: Currently, I am investing only in the Mutual Funds using funds from the NRE bank account.

| Banks / Brokerages | Accounts & Comments |

| Kuvera + MF Central | For Indian Mutual Funds. I invest directly via the respective AMC websites. These accounts are for simply tracking my portfolio and generating consolidated statements for income tax declaration. |

| Zerodha | Non-PIS stock brokerage account for NRIs. Planning to open one soon but nothing urgent because my primary target is exhausting the 150k limit in my French PEA account. |

Emergency Funds & Savings

Living in France provides certain financial stabilities even in the case of some worst life situations like unemployment, unplanned medical emergencies, etc.

- However, an emergency fund with 3-6 months worth of monthly expenses is highly recommended.

- I have kept them in very easily accessible savings accounts, which also offer some very good interest rates of up to 7.25 %. They are divided between India and France.

- This is another reason for keeping a very low balance in my current accounts.

- Various options in France are Livret A, LDDS, LEP, Assurance Vie (Fonds Euro), etc. More details in Banking: Types of Savings Accounts in France.

- Various options in India are Fixed Deposits, Debt mutual funds, etc.

Note: Though NRE FDs are tax-free in India, we have to pay a 30% flat tax (or according to income tax bracket) on the interest income to France.

Equity Investments

Finally, we have arrived at the most important component of my savings and investment portfolio.

- I am a very big believer in equity products and so prefer to have at least 75% of my portfolio invested in ETFs, stocks, mutual funds, etc.

- Most of my investments are usually planned for a very long time and a minimum horizon of 10 years. Also, I have another 30+ years for retirement.

- Though I have a very big risk appetite, I am neither interested in penny stocks nor meme-coins planning for the moon.

- Except a few quality dividend stocks in my PEA account, most of my equity investments are boring passive funds: Index ETFs and Mutual Funds.

PEA – Plan d’épargne en actions: PEA is one of France’s best investment options available to tax residents. However, many people start directly with a regular brokerage account (CTO) and do not take advantage of certain tax benefits.

- Contains around 40% of my total portfolio.

- A PEA account allows us to invest in French and European stocks while benefiting from certain tax advantages.

- There are no yearly taxes on capital gains and dividends, as long as we do not withdraw our funds from the account.

- Limited to 1 account per tax resident in France and the total investment limit is capped at 150k euros. However, this limit does not apply to the capital gains and dividends earned inside the account.

- After 5 years of account opening, only the social charges of 17.2% are applicable on the capital gains instead of the usual 30% flat tax or taxed according to your tax bracket. My PEA account will be 5 years old in April 2025.

- However, there is no tax advantage when the funds are withdrawn before the end of 5 years. Also, the account will be closed.

- I have set up a monthly auto-debit from my bank account to the PEA account and manually invest almost every month.

- More details in Plan d’épargne en actions (PEA): Is it the best investment option in France?.

| Stocks & ETFs | Weightage in Dec’24 |

| Amundi MSCI World UCITS ETF – EUR (C) | 45% |

| Amundi PEA US Tech ESG UCITS ETF Acc | 35% |

| European Dividend Stocks | 20% |

- Recently, Amundi updated a few ETFs like Nasdaq100, etc, and oriented them towards ESG themes (Environmental, Social, and Governance). What Is Environmental, Social, and Governance (ESG) Investing?

- You can learn more about the MSCI World index here ETF – MSCI World Index – Invest In 23 Developed Countries In A Single Transaction

Assurance Vie: Assurance Vie is one of the most used investment products in France, especially to transfer wealth between generations and also benefit from the annual tax rebates.

- It is not a Life Insurance product. A commonly misunderstood part by a lot of people.

- Tax advantage after 8 years of account opening and the investments can be withdrawn anytime.

- I had an account with Bourso Bank but I closed it. When my PEA account crosses 100k euros in investments, I will gradually start focusing on this product.

- You can find more details here What is an assurance-vie?.

CTO – Compte Titres Ordinaire: A CTO is a basic stock brokerage account without any specific tax advantages.

- It is useful for investing in stocks and ETFs not trading on Euronext. Of course, you can use the CTO account for Euronext stocks too but a PEA is a better option.

- Some brokers allow automated monthly investments.

- I have finally settled with Trade Republic because free savings plan after personally exploring other brokers like Interactive Brokers , DEGIRO, Etoro, Trading212.

- Until Dec 2022, I had a 2k euros CTO portfolio with 18-20 American dividend stocks. But, I liquidated the account and transferred all the funds to my PEA account.

- In 2024, I restarted using my CTO account for investing in 2 Chinese ETFs. But the monthly investments are very small wen compared to my PEA allocation. Investing in China is a contrarian strategy and carries a lot of risks.

| Stocks & ETFs | Weightage in Dec’24 |

| iShares MSCI China USD ETF (ACC) | 50% |

| iShares MSCI China A USD ETF (Acc) | 50% |

Mutual Funds in India: Even though I do not live in India now, I completely believe in the India growth strategy. So, I removed the Emerging Markets ETF from my portfolio and reallocated completely towards the mutual funds in India.

- I follow a mixed strategy of automated monthly SIPs (like DCA) in these funds and also do lump sumps manually whenever possible.

- It is a small component of my overall investment portfolio.

| Indian Mutual Funds | Weightage in Dec’24 |

| UTI Nifty Index Fund-Growth Option- Direct | 50% |

| Tata Digital India Fund Direct Growth | 48% |

| HDFC NIFTY Midcap 150 Index Fund – Direct – Growth | 1% (new) |

| UTI Nifty Next 50 Index Fund – Direct Plan | 1% (new) |

Real Estate Investments

As my focus is on equity products, I haven’t touched real estate side until the last quarter of 2024. For choosing any investments, I have a basic thumb rule of making at least 4-5% returns after all deductions. What is the point of investing?, if the returns don’t even beat inflation. So, I chose the SCPI route for getting some passive rental income from real estate.

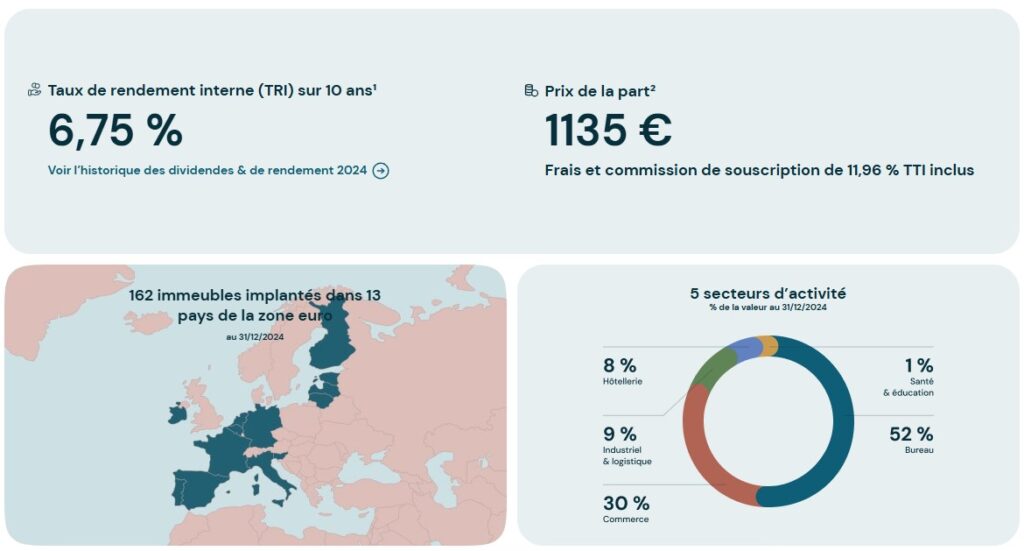

- A SCPI (Société Civile de Placement Immobilier) is a collective investment vehicle dedicated for rental property investments. Also known as Pierre Papier in French, it can include office buildings, retail properties, warehouses, healthcare facilities and residential apartments, etc.

- I chose CORUM Origin SCPI from CORUM L’Épargne based on its performance since inception. It has a diversified real estate portfolio of 162 buildings in 13 European countries and current occupancy rate of 97%.

- Its last 10 years XIRR (TRI-Taux de Rendement Interne in French) is 6.75%. Even during the current real estate crisis in France, it has performed very well.

- Each year for more than 12 years, CORUM Origin SCPI has met or exceeded its annual return target of 6% (unguaranteed and net of subscription and management fees).

- For more details about SCPI, please refer to SCPI: investissez dans l’immobilier avec un placement collectif.

- This real estate investment is very new and so very small part of my portfolio. After a lumpsum investment for opening the account, I have set up a small monthly SCPI investment plan.

- Its biggest advantage is the possibility of getting a bank loan and using the leverage concept similar to buying an actual property using a loan. I do no- have any immediate plans but I will do it whenever possible depending on the interest rates.

- If you would like to invest in SCPIs of CORUM, you can use my referral code MKFB20 and receive a bonus of up to 3% of your initial capital invested. Enter the above code in J’ai découvert CORUM L’Épargne >> Programme de parrainage during your SCPI subscription on epargne.corum.fr/scpi-particuliers/intro.

Retirement Account

An introduction to the French retirement system is explained on the CLEISS website. “In France, private-sector employees’ basic pensions are topped up by the compulsory supplementary pension scheme Agirc-Arrco, which is also financed on a pay-as-you go basis.” The detailed article from CLEISS explains this topic The French Social Security System III – Retirement

- You can find your pension retirement rights, do simulations of retirement pension, trimesters accumulated, etc via the govt website www.lassuranceretraite.fr

- In addition to this mandatory pension scheme, it is good to invest in your own private retirement savings account like PERin explained below.

PERin – Plan d’épargne retraite individuel: Target date mandate system and so currently investing 100% into equity ETFs with 54% of funds invested in Europe.

- Will automatically rebalance to 100% debt towards retirement age.

- Highly recommended for people in the 30% tax bracket (TMI) and above.

- May not be useful for people in the 11% tax bracket and below.

- Reduces Tax now but the funds are blocked until retirement.

- Only account which is under “Gestion pilotée” mode. It means that investment options like ETFs, bonds, etc are chosen by the brokerage according to our risk profile.

- I have explained about PERin with all the details here PER – Plan Epargne Retraite : French Retirement Savings Account And Tax Reduction

Pension from French Government: To be entitled to the French social security retirement pension, we must have contributed at least 1 quarter as an employee (or business). A quarter or trimester means a duration of 3 months. For every year of work, 4 quarters are added to our French retirement account irrespective of our nationality.

- To understand your eligibility, please refer to What is the minimum duration required to qualify for pension in France?.

- To go on full retirement, I need 172 trimesters and I have accumulated 35 trimesters so far until December 2024. My official retirement is more than 30 years away and so not relevant anytime soon.

- You can find your work history, trimesters earned, retirement age, pension amount, simulate your retirement, etc. in your official retirement account and on lassuranceretraite.fr

Crypto Investments

I have been investing in cryptocurrencies since 2021. So, I have seen huge oscillations (volatility) on both sides and this helped in knowing by overall investment risk appetite.

- In 2024, I have not added any funds but the weightage increased to 22% of total portfolio due to the current crypto market conditions.

- I do not DCA into cryptocurrencies but invest during the bear markets.

- Staking generates additional value to the portfolio. It is like bank interest.

- Will reduce the exposure back to 5-10% whenever possible and move funds to the PEA account.

- I had the portfolio in Binance until June 2023 but I have transferred everything back to Kraken.

- Cryptocurrencies are one of the most volatile investments. So, I invest mostly in BTC, SOL, ADA, ETH and XRP. For booking profits, I use USDC stable coin.

- These are some of the top currencies based on market cap and I do not get into any meme coins or the ones planning for the moon.

- In France, there is no taxable event as long as cryptocurrencies are not converted into fiat currencies (USD, EUR, etc).

- When these crypto investments are converted back into Euros, a flat tax of 30% is applicable.

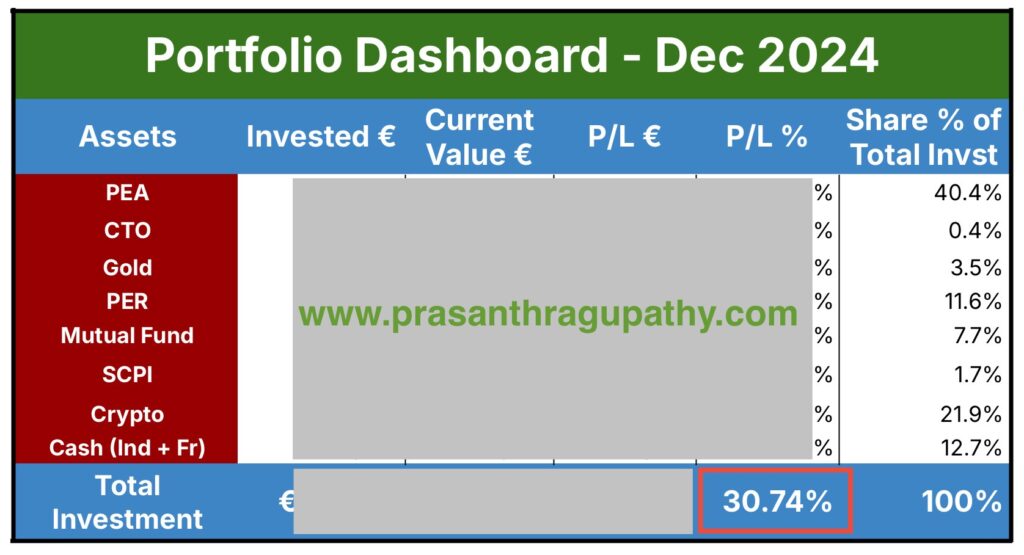

Portfolio Dashboard – Dec 2024

Here is the overall view of my savings and investment portfolio until December 2024. I try to do a yearly review of my portfolio performance and update this article. This is the 3rd version since 2022 and overall portfolio performance is currently around 30%.

For benchmarking my portfolio, I use the performance of MSCI World Index. More details about this index on ETF: MSCI World Index – Invest in 23 developed countries in a single Transaction.

| Annualized Performance of Index until Dec 2024 | ||

| Timeline | Amundi MSCI World UCITS ETF – EUR (C) | MSCI World Index |

| 1 Year | 27,15% | 27,45% |

| 3 Years | 12,94% | 13,11% |

| 5 Years | 12,67% | 12,81% |

| 10 Years | 11,22% | 11,32% |

Income Tax Declaration

As someone doing savings and investments in two countries, I complete my annual income tax declarations in France and India. So, understanding the Double Tax Avoidance Agreement (DTAA) between France and India becomes very important, Declaration of Indian Income in France based on DTAA. Unfortunately, I haven’t yet found a professional who is competent in taxation matters involving these 2 counties. So, I had to learn it on my own.

France: Income tax declarations in France are done every year between April to June, depending on where we live in France or its foreign territories.

- Revenu fiscal de référence (RFR) available from the tax returns Avis d’impôt is used to calculate the eligibility criteria for so many social benefits in France.

- This is another important reason why I keep encouraging even students to submit an income tax declaration.

- A few helpful articles and videos on taxes written so far on this blog are added below.

India: I submit income tax declarations online before 31st July every year.

- ITR-2 for NRIs not having income under the head Profits and Gains of Business or Profession. This is my case.

- ITR-3 for NRIs having income under the head Profits and Gains of Business or Profession.

- If you are living abroad but have some investments in India or going to inherit something in the future, it is highly recommended to do an income tax declaration.

- If you are not earning anything currently in India, you can still submit a zero-income tax declaration. ITR2 hardly takes 5 minutes to complete and it will be helpful in the future.

- For more information, Returns and Forms Applicable for Non-Resident Individual

Assumptions & Notes

This portfolio includes only the savings and investments done using my salary income. It does not include any inheritance from the family.

- The average EUR-INR Rate used is 90 rupees for 2024. For French income tax declaration, the official rates from Banque de France website must be used.

- Annual Inflation Growth at 6% for expenses and expected CAGR of 12% for total portfolio.

- Blocked funds can be withdrawn earlier, based on some specific reasons.

- I have not mentioned the % of capital invested, profit/loss info, CAGR, etc.

- Took me 3 years to understand various things and countless discussions with a few ppl. Includes a lot of trial/error over these years to finally arrive at this portfolio.

- I don’t know where I will be after 3-5 years. So, no point in pondering too much about it. Wasted some precious time thinking about these things.

- Knowing French helped a lot, especially in understanding the French tax calculations & financial documents.

- Couples should figure out their risk capacity together. So, I might have to consider it when I get married & patiently explain all these things to my future partner. This is very important and will have a huge impact on the financial situation. I have seen so many couples struggling with this aspect.

Thanks for reading until here. Feel free to add your suggestions, questions, etc. in the comments.

Support This Blog!

If you’ve found my articles helpful, interesting or saving your time and you want to say thanks, a cup of coffee is very much appreciated!. It helps in running this website free for the readers.

DISCLAIMER

Any finance-related information shared is not professional legal, tax, or investment advice. The information provided is of an educational and general nature and is not investment advice within the meaning of Articles L. 321-1 and D. 321-1 of the French Monetary and Financial Code. Investment carries risks of loss and past performance does not guarantee future performance. Please consult a registered CGP/CIF for professional financial advice.

Hey prasanth, thank you for this post.

May I ask

1) if Livret A is a good instrument to park emergency fund? Boursorama gives 3% on the deposits. Or would you suggest some other instrument?

2) any reason you switched from binance? I use the same.

3) how do you manage dividends? Do you reinvest them?

4) would you refer some resources for tax filing? I’m not sure how do I include taxes on dividends gains, livret A gains etc.

Thanks

Hello Akash,

The idea behind writing this article is to list the various savings/investments options, share personal experiences and create awareness about personal finance. It is not meant for individualized personal finance advice as explained in the disclaimer.

1. Please use the suitable savings option from the list https://prasanthragupathy.com/2023/12/banking-savings-accounts-in-france/ Some are tax-free and some are taxed.

2. CZ’s arrest and fine of billions was an important reason.

3. Yes, dividends are re-invested.

4. Probably, you have missed my posts about income declaration last year. Please check my Step-by-step tutorials on Income Tax declaration in France https://prasanthragupathy.com/2024/05/tax-step-by-step-tutorials-on-income-tax-declaration-in-france/

Cheers,

Prasanth

Hello ,

Thank you so much for the article. It was very informative. I have found most of my doubts regarding investing in France.

I have only one doubt regarding crypto. If I convert my crypto to stable coin like USDC . Do I have to pay tax for that or only when I cash out?

Hello Shravan,

Stablecoins like USDC and USDT are cryptocurrencies too and not Fiat ones. For example:

– If you convert BTC to USDC, it is not a taxable transaction.

– If you convert BTC or USDC to EUR, it is a taxable transaction. Even in this situation, only profits from 305 euros and above (2024 value) are taxable in France.

Hi Prasanth,

Thanks for the information. I would also like to know about capital gain tax on stocks invested in India. Do we also have to pay tax in France?

Hello Shravan,

If you are tax resident in France, capital gains from movable assets in India will be taxed in France. You can choose between a 30% flat tax or taxed according to your income tax bracket.

If any tax is paid in India including TDS, a tax credit of max 10% is possible in France.

Cheers,

Prasanth

Hi Prasanth ! Thankyou for the detailed posts.

I’ve relocated 6 months ago and am yet to make my first income tax declaration (been told I have to do it next year). However I am being taxed at source already. Point is – I don’t have a numero fiscale and want to open a PEA.

Will not having one right now – impact my potential PEA opening ? Or are there ways I can open it and start running it and link my tax number later ?

Hello Anne,

If you had moved to France in 2025, the tax declaration advice is correct.

A PEA account can only be opened by tax residents in France and so you are eligible too. You can submit a request for PEA account opening using a ID proof (passport & visa), recent address proof and French Bank RIB. Feel free to use the referral codes in the above article.

Cheers,

Prasanth

PS: If my articles and answers are helpful, please leave your feedback on Trustpilot

Hi Prashant,

First of all, I really appreciate your work your blog is super helpful.

I have a question about my situation. I’ve been in Paris for a year as a student. I opened a CIC account, but after 6 months they suddenly closed it without giving me a proper reason. Later, BNP also rejected my application.

Since then, I’ve been using Revolut for my salary and daily expenses. Based on what you mentioned in your article, can I open an account with Boursorama or Hello Bank and rely fully on online banks instead of going for traditional banks like LCL or Société Générale? Also, will there be any issue if I submit online bank statements when renewing my visa?

Hello Mohammad,

As explained in the portfolio audit article above, I am with 100% online banking (France HQ banks) since 2018. These are proper French banks and so there will not be any issues. I have a Revolut account but it does not fall in the same category as Hello or Bourso banks.

Cheers,

Prasanth

PS: If my articles and answers are helpful, please leave your feedback on Trustpilot