Published on: February 26, 2026 | Article No: 345 | By: @rprasanth_kumar

French income tax brackets and rates are updated every year. For example, the 2026 tax rates applied to income earned in 2025 are set by the 2026 Finance Law LOI n° 2026-103 du 19 février 2026 de finances pour 2026.

To account for inflation, the 2026 income tax brackets were raised by 0.9% compared to 2025.

- If your income increased by less than 0.9%, you will pay less tax.

- If your income increased by about 0.9%, your tax will be roughly the same as in 2025.

- If your income increased by more than 0.9%, you will likely pay more tax.

Table of Contents

- Income Tax Rates – Barème de l’impôt 2026

- Family Quotient

- How to calculate your income tax and some examples?

- Single without children

- Couple without children

- Couple with 1 child

- Official Income Tax Calculator

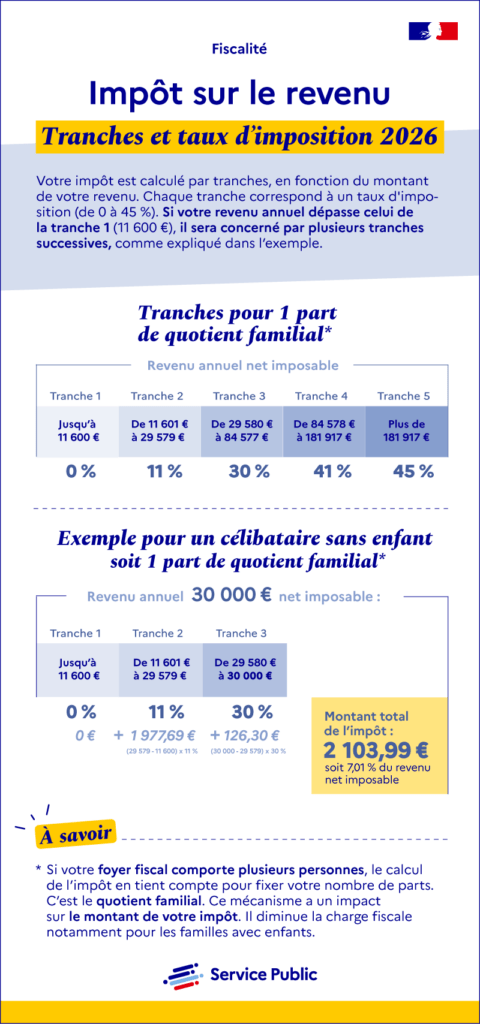

Income Tax Rates – Barème de l’impôt 2026

The following table explains the income tax brackets tranches d’imposition and tax rates taux d’imposition applied to your income earned from January to December 2025.

The income mentioned in the below table is after removing the 10% standard deduction or the actual professional expenses “frais réels“. To know more about these deductions, Impôt sur le revenu – Frais professionnels: forfait ou frais réels (déduction)

| 2026 Income Tax Brackets | Tax Rates |

| Up to €11,600 | 0 % |

| €11,601 to €29,579 | 11 % |

| €29,580 to €84,577 | 30 % |

| €84,578 to €181,917 | 41 % |

| Above €181,917 | 45 % |

Family Quotient “Quotient Familial”

According to Article 193 of the General Tax Code (CGI), the family quotient is a system that divides the total taxable income into several shares or parts of the family. Based on the taxpayer’s personal and family circumstances and the number of dependents, the family quotient is used to define the income that serves as the benchmark for determining the amount of income tax.

Some examples:

- If you are single, divorced, or widowed, without dependent children, you will have only 1 part of the family quotient.

- If you are married or PACSed, without dependent children, you will have 2 parts of the family quotient.

- If you have dependent children, you can benefit from additional family quotient parts.

- If you are disabled or a veteran, you can also benefit from additional family quotient parts (Article 195).

Attention: The Quotient Familial used by the tax office is different from the one used by CAF. For more information, Quotient familial : Caf, impôts, quelles différences ?

Number of children under your charge | Number parts by Family Quotient | |

| Single or Divorced | Married or PACSed Couple | |

| 0 | 1 | 2 |

| 1 | 1.5 | 2.5 |

| 2 | 2 | 3 |

| 3 | 3 | 4 |

| 4 | 4 | 5 |

| per additional child | +1 | +1 |

How to calculate your income tax?

The income tax is calculated from our net taxable income revenu net imposable (RNI), in 3 major steps.

- Divide the net taxable income (RNI) by the number of family members quotient familial.

- Then apply this value to the income tax brackets and income tax rates from the above table.

- Multiply the result by the number of parts in the quotient familial to obtain the amount of tax. This is the Gross Tax Impôt Brut (IB) to be paid by the household.

Note: The Net Tax Impôt Net (IN) to be paid can be obtained by subtracting the various tax credits and reductions from the Gross Tax.

Here are a few example calculations of Income tax in France, based on the number of taxable people in the family.

Example 1: Single person with net taxable income of €30,000 in 2025

Step 1: If you are a single, unmarried, divorced, or widowed person without children, the number of parts in your family quotient is 1.

- So, 30,000 € / 1 = 30,000 €.

Step 2: Then apply this value to the income tax brackets and tax rates of 2026, applicable to the income earned during 2025.

| Income Tax Brackets | Tax Rates | Tax to be paid |

| Up to €11,600 | 0 % | 0€ |

| €11,601 to €29,579 | 11 % | (29,579 – 11,600 x 11 % = €1977.69 |

| €29,580 to €30,000 | 30 % | (30,000 – 29,579) x 30% = €126.30 |

| Total | 1977.69 + 126.30 = €2,103.99 | |

Step 3: To find the tax that you have to pay on your income, you should again multiply this value by the number of parts, family quotient.

- €2,103.99 x 1 = €2,103.99. This is the Gross Tax Impôt Brut (IB) to be paid by the household.

So, this person falls in the 30% tax bracket Taux Marginal d’Imposition (TMI). However, not all of the income is taxed at 30%. The overall average tax rate Taux Moyen d’Imposition for this person is 7.01% (2,103.99 ÷ 30,000).

Example 2: Married or PACSed couple without children and a net taxable income of €60,000 in 2025

Step 1: If you are a couple without children, the number of parts in your family quotient is 2.

- So, €60,000 / 2 = €30,000.

Step 2: Then apply this value to the income tax brackets and tax rates of 2026, applicable to the income earned during 2025.

| Income Tax Brackets | Tax Rates | Tax to be paid |

| Up to €11,600 | 0 % | 0€ |

| €11,601 to €29,579 | 11 % | (29,579 – 11,600 x 11 % = €1977.69 |

| €29,580 to €30,000 | 30 % | (30,000 – 29,579) x 30% = €126.30 |

| Total | 1977.69 + 126.30 = €2,103.99 | |

Step 3: To find the tax that the couple have to pay on their income, they should again multiply this value by the number of parts, family quotient.

- This tax is multiplied by the number of household shares. In this example, it is multiplied by 2.5

- So, €2,103.99 x 2 = €4,207.98. This is the Gross Tax Impôt Brut (IB) to be paid by this household of 2 people.

So, the couple fall in the 30% tax bracket Taux Marginal d’Imposition (TMI). However, not all of the income is taxed at 30%. The overall average tax rate Taux Moyen d’Imposition for this couple is 7.01% (4,207.98 ÷ 60,000).

Example 3: Married or PACSed couple with 1 child and a net taxable income of €90,000 in 2025

Step 1: If you are a couple with 1 child, the number of parts in your family quotient is 2.5. It means 1 part for each parent and 0.5 part for the child.

- So, €90,000 / 2.5 = €36,000.

Step 2: Then apply this value to the income tax brackets and tax rates of 2026, applicable to the income earned during 2025.

| Income Tax Brackets | Tax Rates | Tax to be paid |

| Up to €11,600 | 0 % | 0€ |

| €11,601 to €29,579 | 11 % | (29,579 – 11,600 x 11 % = €1977.69 |

| €29,580 to €36,000 | 30 % | (36,000 – 29,579) x 30% = €1926.30 |

| Total | 1977.69 + 1926.30 = €3,903.99 | |

Step 3: To find the tax that the couple have to pay on their income, they should again multiply this value by the number of parts, family quotient.

- This tax is multiplied by the number of household shares. In this example, it is multiplied by 2.5 because the couple is married (or in a civil union) and with a child. Initial tax calculation: €3,903.99 × 2.5 = €9,759.97.

- Normally, A couple without children earning €90,000 would pay €13,207.98 in tax.

- The tax advantage from having one child is: €13,207.98 − €9,759.97 = €3,448.01.

- But, the maximum allowed child tax benefit is €1,807 (family quotient cap). So, €3,448.01 − €1,807 = €1,641.01.

- Final tax for the couple with one child after considering the tax benefit: €9,759.97 + €1,641.01 = €11,400.98 instead of €13,207.98.

So, the couple fall in the 30% tax bracket Taux Marginal d’Imposition (TMI). However, not all of the income is taxed at 30%. The overall average tax rate Taux Moyen d’Imposition for this couple is 12.67% (11,400.98 ÷ 90,000).

Income Tax Calculator in France

2026 Income tax simulator is not yet published. This article will be updated whenever the simulator is available.

Here is the official 2025 income tax calculator for 2024 income to estimate your tax amount and reference tax income (revenu fiscal de référence).

The simulator is useful only for residents of France and has two versions:

- Simplified model: For those reporting only salaries or pensions and common deductions such as child support, childcare costs, donations, etc.

- Complete model: For those with additional income sources such as business, freelance, agriculture, overseas investments, deficits, etc.

Source: Service-public.fr

DISCLAIMER

Any finance-related information shared is not professional legal, tax, or investment advice. The information provided is of an educational and general nature and is not investment advice within the meaning of Articles L. 321-1 and D. 321-1 of the French Monetary and Financial Code. Investment carries risks of loss and past performance does not guarantee future performance. Please consult a financial advisor for any professional advice.